The £300 Billion Trade Question

What US Tariffs Mean for UK Brands Right Now

The US is the UK’s single biggest trade partner. With new tariffs incoming, what’s at stake - and what should retail operators and supply chain leaders do next?

In 2023, the UK exported £187 billion worth of goods and services to the United States. That’s 22% of all UK exports. Imports from the US totalled £115 billion, or 13% of all UK imports. It’s a relationship worth over £300 billion—a lifeline for many retail and e-commerce brands.

But now, that lifeline comes with a catch.

The US administration has announced new tariffs on imports from key trade partners, including the UK. A blanket 10% on a wide range of products, with specific sectors facing duties up to 25%. What began as policy murmurs is now material impact.

If your business ships to the US, you’re exposed. And even if it doesn’t, you’re likely downstream of someone who is.

The New Rules of Play

The US has officially imposed a 10% tariff on UK-origin goods, with sectors like automotive and metals taking a steeper 25% hit. Meanwhile, the de minimis threshold, which has long allowed UK brands to ship low-value goods duty-free to US consumers, is firmly in the political crosshairs. An executive order has now been signed to eliminate this exemption for low-value imports from China and Hong Kong, effective May 2, 2025. While this doesn't yet apply to UK shipments, it sets a clear precedent, and a warning shot.

We called this months ago. When both sides of the US political aisle start eyeing the same policy lever, it stops being theoretical.

Mapping the Exposure

The UK is still a service-led economy; 54% of exports and 35% of imports in 2023 were services. But it’s physical products that are under the cosh here.

To put it in context:

The US accounted for 15% of UK goods exports in 2023.

10% of the UK's imported goods came from the US.

Scotch whisky? On the line.

Fashion and lifestyle brands with fulfilment operations in the UK? Directly affected.

Electronics and automotive components? Squarely in the firing line.

While the Commons Library data shows that UK trade in real terms has flatlined since 2019, the composition of that trade is shifting. With Asia trade falling and EU volumes plateauing, more businesses have looked to the US as a growth market. That market is now looking a lot more expensive.

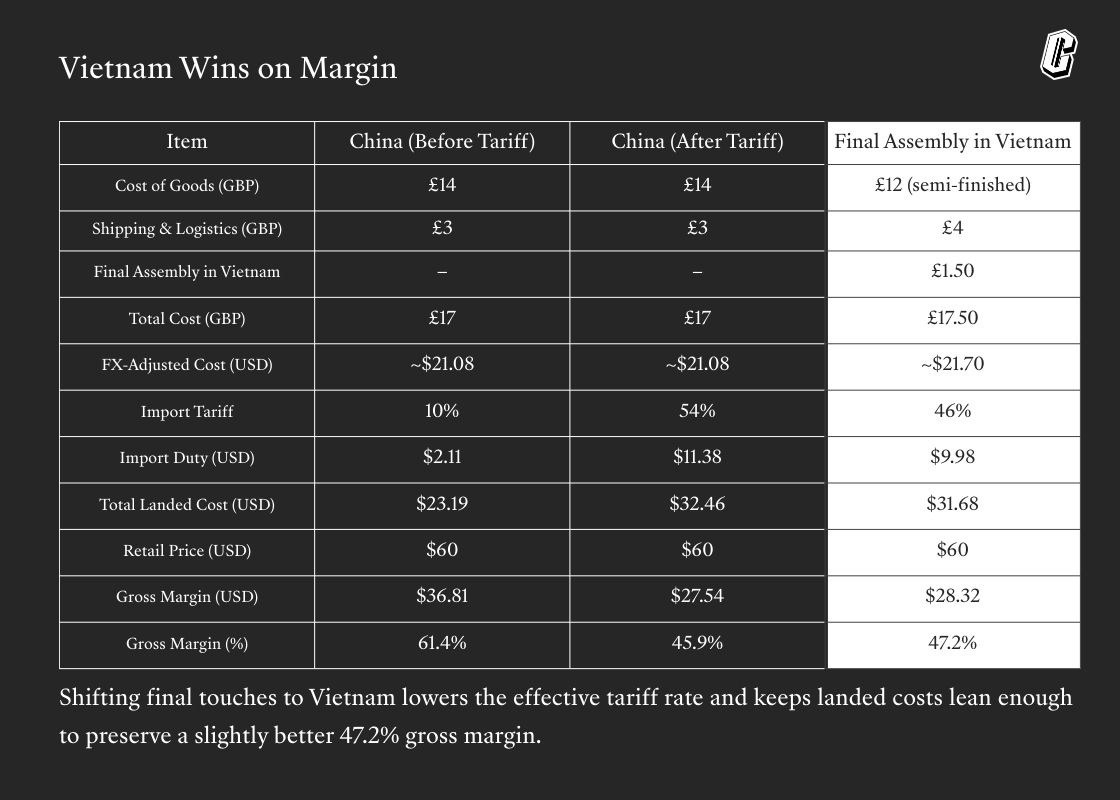

Strategic Shifts in Manufacturing

One increasingly common move? Brands shifting the final stages of manufacturing or finishing processes to countries with more favourable tariff arrangements. By doing so, they can legally classify goods as being made in a different country, one with lower duties, thereby reducing the landed cost when those goods enter the US market.

It’s not a silver bullet, but for some products, adjusting the country of origin by altering where they’re assembled, labelled, or finalised can make a measurable difference on duty rates. We’re seeing everything from relabelling to full packaging operations being relocated to take advantage.

As tariff regimes become more fragmented, smart brands are reworking not just what they make, but where they finish it.

Do Nothing, Pay More

The most common response we’ve seen from UK brands? Wait and see. That was understandable six months ago. It’s no longer a viable strategy.

Doing nothing now means:

You absorb the cost (margin killer)

You pass on the cost (conversion killer)

Or you lose share to a competitor who moved faster

Brands that have started scenario-planning are looking at:

Re-routing fulfilment to US warehouses

Splitting inventory into US-destined and RoW stock to manage tariffs more intelligently

Repricing SKUs and creating "US editions"

Lobbying shipping partners for better landed cost options

This Isn’t Just About America

The real story here isn’t just US protectionism. It’s the new reality of friction-filled global trade. China trade is down 20% YoY. EU trade is stable, but sluggish. Brands banking on simple, seamless global logistics are waking up to a very different landscape.

If the world’s biggest buyer and the UK’s largest single export partner starts charging you more to play, you can’t afford to sit on the sidelines.

What Now?

You don’t need to panic. You do need a plan.

Start by:

Mapping SKUs by margin and tariff exposure

Building US-specific pricing models

Reviewing de minimis-dependant workflows

Rethinking what goes into your US-bound inventory

This is the kind of work that separates operationally excellent brands from the rest. Because tariffs aren’t just a policy change. They’re a filter.

And the brands that pass through? They’ll be the ones who saw this coming and got ahead of it.

If you want help scenario-planning your tariff exposure or reworking your ops stack to handle it, you know where to find us.